Canada is transforming its retirement framework by offering seniors two flexible federal options that go beyond the traditional retirement age of 65. Historically, Canadians associated age 65 with automatic eligibility for key federal programs like Old Age Security (OAS) and the Canada Pension Plan (CPP). But now, older adults can personalize their retirement plans based on their financial goals, health, and lifestyle. This guide explores these new choices, how they impact government benefits, and how Canadians can better plan for their retirement income moving forward.

Canadian Seniors Can Now Delay Retirement

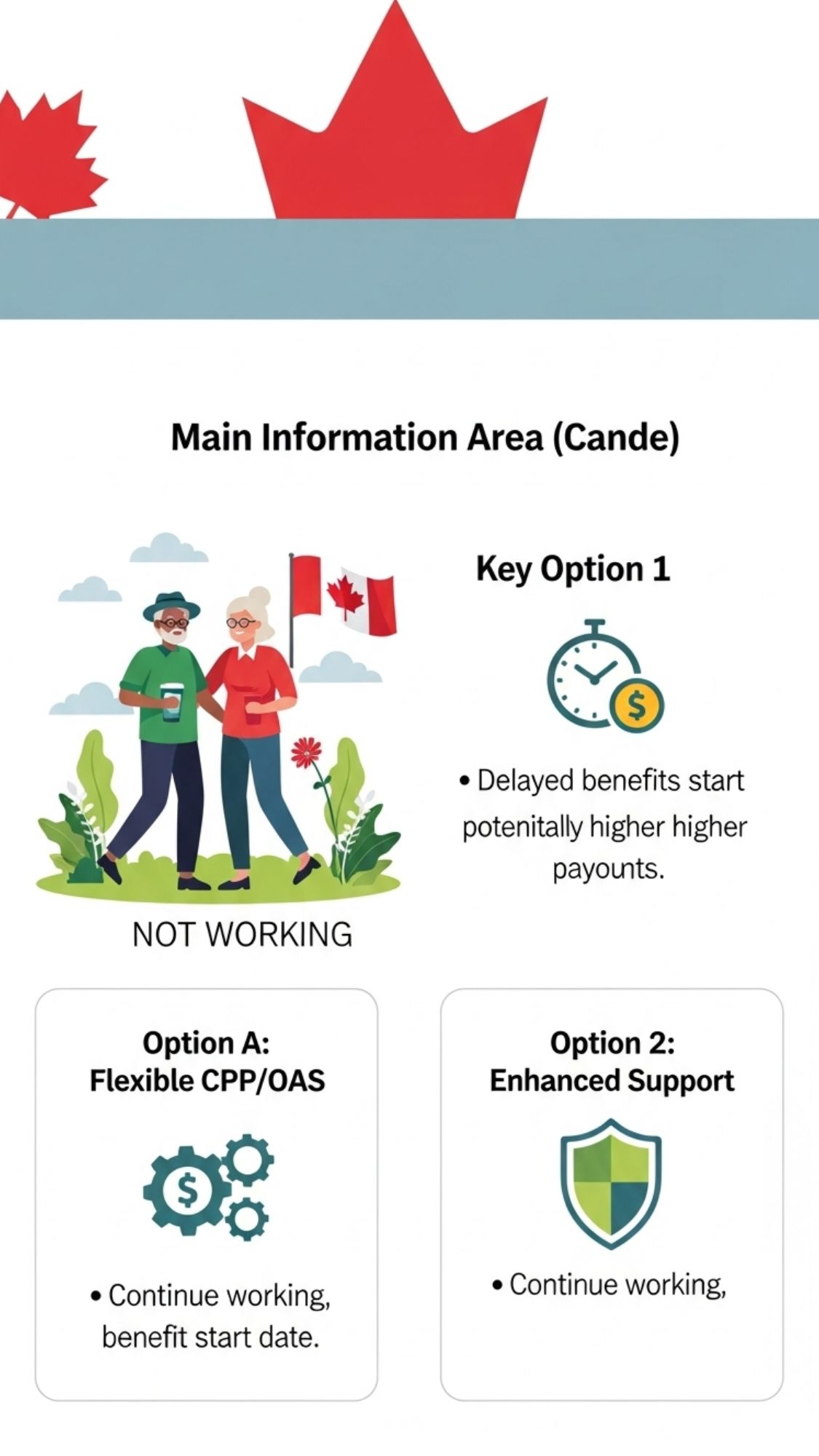

Under the first federal option, Canadians can choose to delay retirement beyond age 65 while deferring CPP and OAS benefits. For CPP, deferring past 65 can increase payments by 0.7% per month, up to a total of 42% by age 70. Similarly, delaying OAS boosts payments by 0.6% monthly, or 7.2% annually. This strategy suits seniors who are still in good health, financially secure, and looking to maximize lifetime income. It also allows seniors to remain employed—either full-time, part-time, or self-employed—while tailoring benefit timing to suit long-term needs.

Urgent: Expired ID Holders Face Grant Cut-Off Starting 28 December - Reverification Required!

Urgent: Expired ID Holders Face Grant Cut-Off Starting 28 December - Reverification Required!

Option Two: Partial Retirement With Income Flexibility

The second option is partial retirement, allowing seniors to combine work with partial CPP or OAS benefits. This approach helps reduce the financial shock of stopping work abruptly. Seniors can continue part-time employment while accessing part of their pension, giving them income stability and greater control over cash flow. It’s ideal for those who wish to stay active, maintain social networks, and ease into retirement gradually. Importantly, this strategy helps avoid immediate clawbacks and supports a more manageable tax profile.

How the CPP Program Is Affected

The Canada Pension Plan (CPP) has always offered flexible timing. Canadians can begin CPP as early as age 60 (with a reduction), take it at 65 (standard), or delay until age 70 (maximum payout). The new federal options now structure these choices into a broader retirement strategy. Delaying CPP not only results in higher monthly benefits, but also creates space for individuals to earn income without reducing their pension, if managed well with part-time work or self-employment.

CRA and Service Canada Federal Benefits for 2026: Here Are All the Benefit Payments for Canadians

CRA and Service Canada Federal Benefits for 2026: Here Are All the Benefit Payments for Canadians

OAS Payments and Deferral Impacts

Old Age Security (OAS) remains a core federal benefit that starts at age 65, but now includes a deferral mechanism up to age 70. For each month deferred, payments increase by 0.6%. Higher-income retirees must also consider the OAS recovery tax (clawback), which partial retirement may help avoid by controlling annual taxable income. These new policy shifts make it possible for retirees to optimize their benefit start date while still maintaining employment and financial flexibility.

Key Financial Planning Factors to Consider

When choosing between delayed or partial retirement, seniors should weigh several important factors:

– Health & Longevity: Longer life expectancy favors delaying benefits.

– Income Needs: Partial retirement offers steady income with reduced reliance on savings.

– Tax Strategy: Smart withdrawal planning can reduce tax burdens and avoid benefit clawbacks.

– Estate Planning: Higher lifetime earnings may leave more for heirs.

Social and Lifestyle Benefits of Flexible Retirement

Financial gains aside, flexible retirement provides several lifestyle advantages. Continuing to work supports mental and physical health, preserves social networks, and promotes a sense of purpose. Seniors can design a retirement lifestyle that includes travel, volunteering, family time, or new hobbies—without sacrificing financial security. Partial retirement, in particular, reduces the psychological pressure that comes with a sudden shift into full retirement.

Potential Challenges with the New Options

While these new federal choices offer great flexibility, there are some hurdles seniors should be prepared for:

– Workplace Culture: Some employers may expect retirement at 65.

– Health Issues: Medical limitations could make extended work difficult.

SASSA publishes full December grant schedule – R2 315, R560, and R1 250 disbursements detailed

SASSA publishes full December grant schedule – R2 315, R560, and R1 250 disbursements detailed

– Complex Finances: Mixing work and pension income requires detailed planning.

Steps to Help Seniors Prepare Strategically

– Review your CPP and OAS statements to understand entitlements.

– Speak with a financial advisor about timing strategies.

– Evaluate your health and work capacity to set realistic expectations.

– Plan for tax-efficient withdrawals from pensions and savings.

– Update estate documents and beneficiaries based on your strategy.

Example Scenarios

Case 1: Delaying CPP

Jane turns 65 but delays CPP until 70. Her monthly CPP rises by 42%. She works part-time for five more years, supporting her lifestyle without dipping into savings.

Case 2: Partial Retirement

Mark chooses partial retirement at 65. He draws 50% of CPP and works part-time, balancing income, work-life flexibility, and time for his grandchildren.

Long-Term Policy Impact on Canadian Retirement

Canada’s shift toward flexible retirement recognizes the evolving needs of today’s seniors. These policies offer greater autonomy, enhanced lifetime earnings, and encourage active aging. Employers may begin adapting their HR policies to accommodate older workers who want to stay productive beyond 65. The changes reflect a broader social and economic trend—redefining retirement as a personalized transition rather than a fixed event

Retirement in 2026 is no longer a one-size-fits-all decision in Canada. The introduction of delayed and partial retirement options means seniors can shape their financial future based on what works best for them. With careful planning, Canadians can maximize pension benefits, extend working years if desired, and enjoy a balanced retirement lifestyle. These changes reflect a modern understanding of aging and empower seniors to make retirement a personal journey—not just a policy milestone.