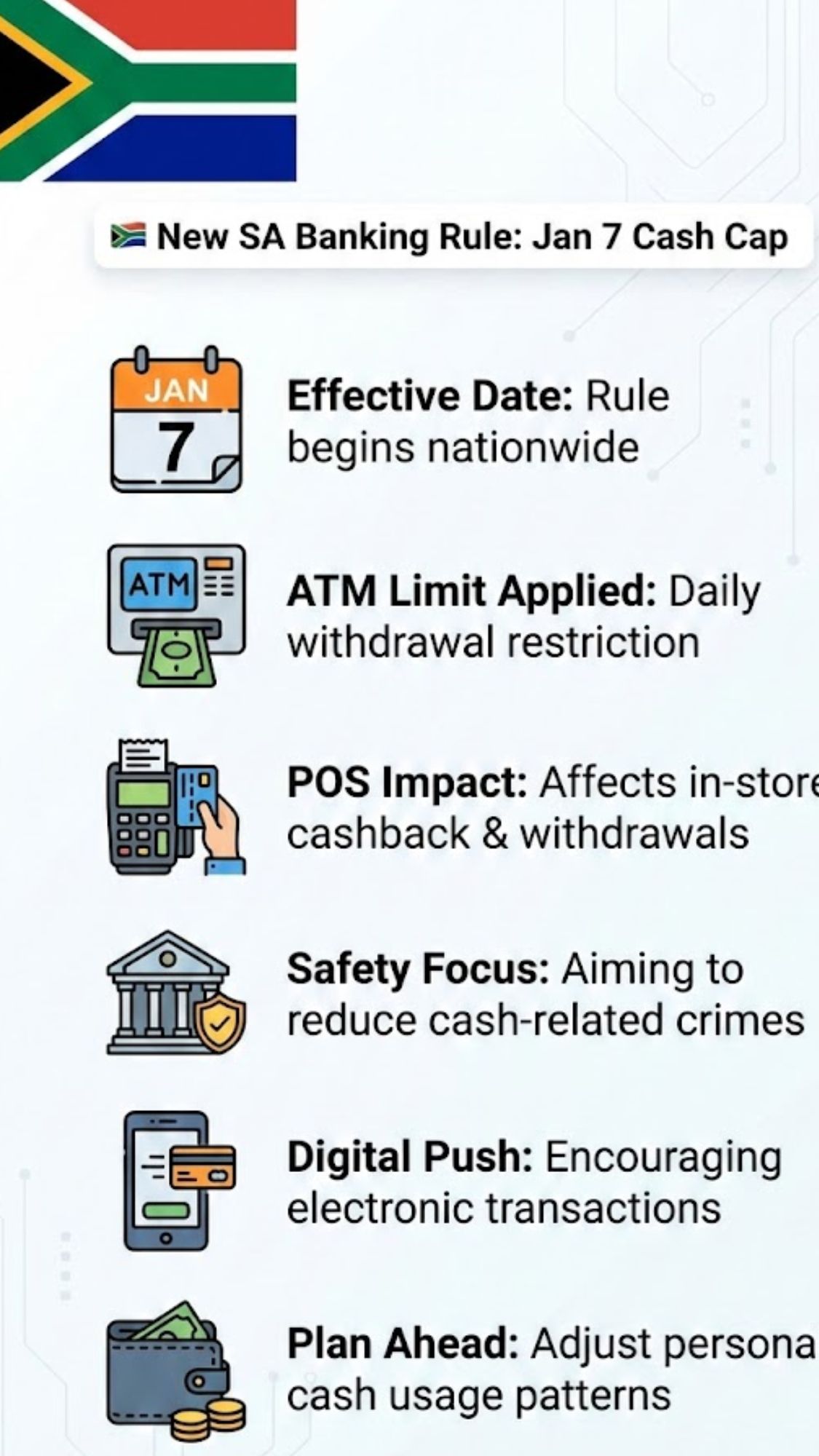

From January 7, 2026, South Africans will encounter new national banking regulations that restrict how much cash they can withdraw daily and weekly from ATMs and debit cards. The South African Reserve Bank (SARB) has worked with major commercial banks to create this cash limit policy aimed at reducing fraud, money laundering and illegal cash dealings. This major change will particularly affect pensioners grant recipients, small business owners and low-income families who depend on cash for their transactions. The withdrawal restrictions apply to all major banks operating in the country such as ABSA, FNB Nedbank, Standard Bank & Capitec. Both urban and rural customers will experience these changes. South Africans should learn about the new daily and weekly withdrawal limits and understand any penalty fees that may apply. They should also look into digital payment options to help them manage their money safely under these new rules.

Why the Government Is Introducing New Cash Withdrawal Rules

The South African government, together with the South African Reserve Bank (SARB), has outlined several key reasons for rolling out this updated banking regulation. The primary aim is to strengthen financial security while modernising how cash is used across the country. Authorities want to limit money laundering activities, reduce illegal cash movements, and improve traceability of large withdrawals. The policy also encourages wider use of digital and card-based payments, lowers ATM replenishment expenses, and cuts down theft-related risks. Importantly, the regulation is designed to protect SASSA grants and pension funds from fraud and organised scams. This shift aligns South Africa with global financial practices where cash usage is capped to support safer, more transparent banking systems.

Updated Cash Withdrawal Limits Explained

The newly introduced withdrawal limits are structured according to account type and customer category. These limits officially take effect from January 7 2026. While exact caps differ across banking profiles, the goal remains consistent: to discourage excessive cash withdrawals while still allowing reasonable access. The revised limits apply to both daily and weekly withdrawals and are intended to balance convenience with security. Banks will communicate the applicable thresholds directly to customers to ensure clarity and compliance under the new framework.

| Account Category | Applicable Bank | Maximum Daily ATM Withdrawal | Maximum Weekly ATM Withdrawal | Daily Card Spending Limit | Total Monthly Cash Cap |

|---|---|---|---|---|---|

| Standard Savings Customers | All Major Banks | R2,000 | R10,000 | R3,000 | R40,000 |

| SASSA Grant Recipients | Postbank / FNB | R1,500 | R6,000 | R2,000 | R25,000 |

| Pension & Retirement Accounts | All Major Banks | R1,000 | R4,000 | R1,500 | R20,000 |

| Business & SME Accounts | Commercial Banks | R5,000 | R25,000 | R10,000 | R60,000 |

| Premium & High-Value Clients | All Major Banks | R8,000 | R40,000 | R15,000 | R100,000 |

| Capitec Global One Account Holders | Capitec Bank | R2,500 | R12,500 | R3,000 | R45,000 |

| Students & Youth Accounts | All Major Banks | R1,000 | R3,000 | R1,500 | R15,000 |

| Senior Citizens (60+) | All Major Banks | R1,200 | R4,500 | R1,800 | R18,000 |

Impact on SASSA Grant Recipients and Pensioners

SASSA beneficiaries and pensioners are among the most impacted by these changes, particularly individuals in rural areas or those without easy access to digital services. The government has confirmed that SASSA cards will continue to function normally for receiving grant payments. The withdrawal caps are meant to prevent large cash-outs that often attract fraud. Notably, card swipes at retail stores and online transactions are not affected by ATM limits. Beneficiaries are encouraged to use Shoprite, Pick n Pay, and Boxer for card-based cash withdrawals, where transaction fees remain minimal.

SASSA Beneficiary Withdrawal Options Under the New System

| Transaction Method | Availability | Maximum Limit | Applicable Charges | Best Usage Advice |

|---|---|---|---|---|

| ATM Cash Withdrawal | Permitted | R1,500 per day | R10 to R25 per transaction | Limit usage to avoid extra fees |

| In-Store Card Payment | Fully Allowed | No fixed limit | Usually free or very low | Recommended for daily shopping |

| Post Office Cash Access | Restricted | Up to R1,000 | Depends on branch rules | Confirm service before visiting |

| Electronic Funds Transfer (EFT) | Available | Up to R25,000 per month | R1.50 to R5.00 per transfer | Ideal for non-cash payments |

| Mobile Cash Send | Enabled | R1,000 per day | Standard bank fees apply | Use only when urgently needed |

Grant recipients will still have access to multiple withdrawal channels, including retail merchant cash-outs and standard card payments. These options are being promoted as safer, cheaper alternatives to repeated ATM withdrawals, especially in high-risk areas.

Penalties for Exceeding the New Withdrawal Caps

South African banks will apply both soft caps and hard caps under the new rules. Soft caps may be exceeded temporarily but will attract additional charges, while hard caps cannot be bypassed. Customers who exceed soft limits may incur penalty fees ranging from R20 to R50 per transaction. Reaching a hard cap could result in a temporary card suspension. Accounts showing repeated high-volume cash activity may be flagged and reported to SARB. Customers expecting unusually high cash needs, such as for funerals or major events, are advised to contact their banks in advance to request temporary exemptions.

How Customers Can Prepare for the Changes

To avoid inconvenience, customers are encouraged to adjust their banking habits early. This includes using digital banking apps to track withdrawals, limiting ATM visits to once or twice per week, and relying more on EFT transfers and mobile wallets. Making purchases through direct card swipes at registered stores is also recommended. Banks are advising customers to ask about merchant cash-out services, which are often more affordable than ATM withdrawals. Those living in rural areas should familiarise themselves with the nearest approved withdrawal points and available alternatives.

Official Statements from Government and SARB

Finance Minister Enoch Godongwana and SARB Governor Lesetja Kganyago have both stressed that the regulation focuses on financial modernisation and consumer protection. According to official data, 60% of fraud cases are linked to large cash withdrawals. Authorities have reiterated their commitment to digitising the economy while ensuring continued access to funds. Postbank and SAPO are actively expanding ATM coverage in rural regions, and a dedicated task force is monitoring public feedback to fine-tune the rollout.

Will the Withdrawal Limits Change in the Future?

Yes. SARB has confirmed that the regulation forms part of a three-phase banking reform plan. The current withdrawal limits will be reviewed every six months. Any adjustments will be based on crime and fraud statistics, public adoption of digital banking tools, and improvements in financial infrastructure within cash-poor areas. As South Africa moves toward stronger digital financial controls, the January 7 withdrawal limits represent a significant shift in how citizens manage their money. Staying informed and adapting early will help customers navigate this transition smoothly.