Canadians getting ready to retire now have more options thanks to updated retirement rules in Canada. The Canada Pension Plan and Old Age Security programs have introduced major changes that started rolling out in 2026. These updates remove the old standard of retiring at 65. People can now choose to begin receiving benefits at 60 or wait until 70 to get much larger monthly payments. This gives retirees more say over their income as both life expectancy and everyday expenses continue to climb. The changes include CPP improvements that became fully active by 2026 & new OAS deferral choices. These reforms aim to replace a bigger portion of what people earned before retiring. Long-term contributors can now receive up to 33% of their previous earnings. Those who reach 75 or older get an extra 10% increase. Service Canada has made the application process easier. Payments now adjust every three months based on inflation to match the Consumer Price Index. In 2026 the maximum CPP payment at age 65 is $1433 per month. OAS payments for people between 65 and 74 start at $727.67 monthly and increase to $800.44 for those 75 and older. The 2026 CPP and OAS rules let people keep working beyond traditional retirement ages without facing penalties. This makes it easier to create a retirement plan that fits individual needs and circumstances.

How the Canada Pension Plan Evolved Under the 2026 Flexible Retirement Framework

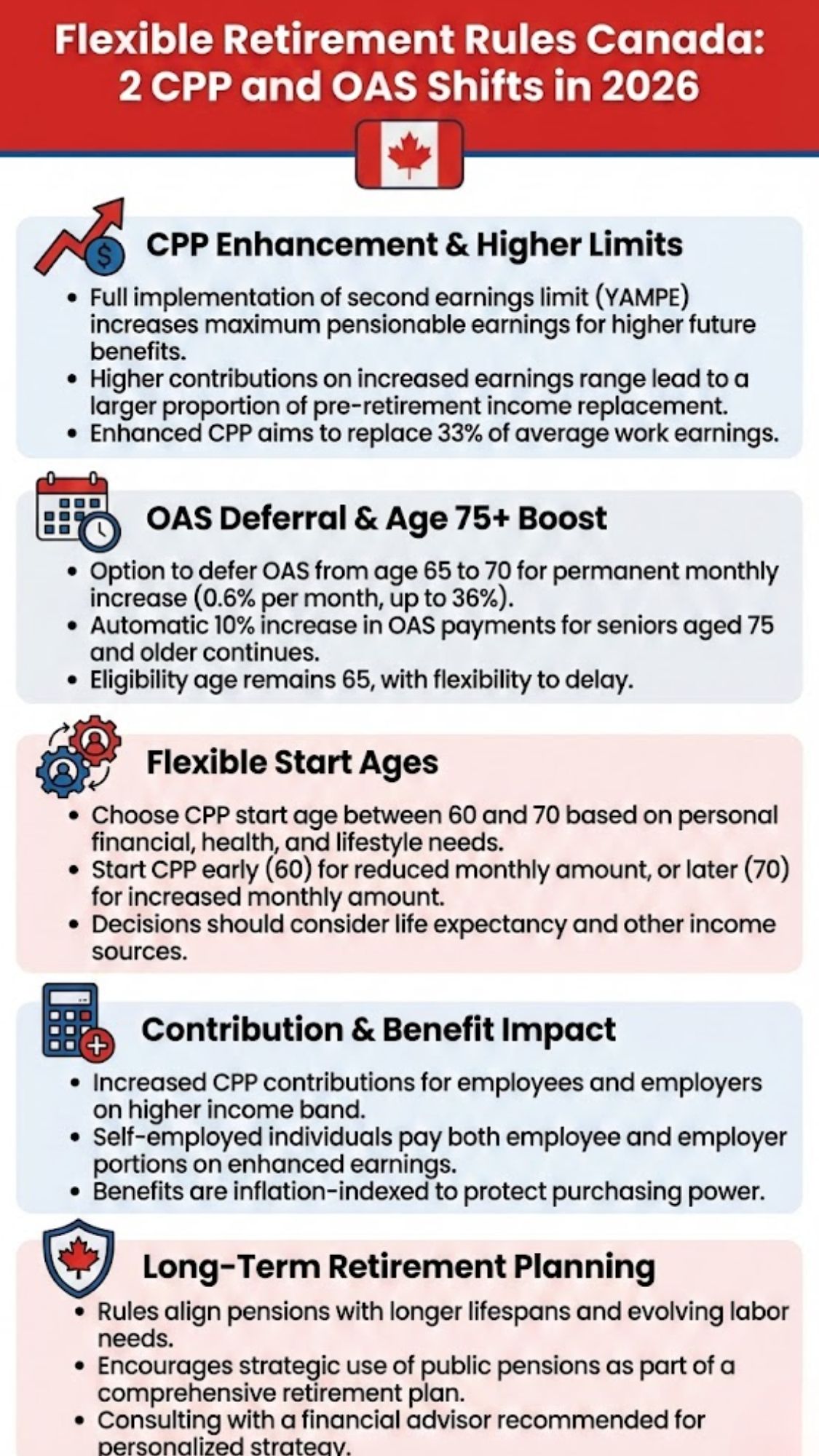

The Canada Pension Plan (CPP) has completed a multi-year enhancement cycle, fully implemented in 2026, reshaping it into a stronger foundation for retirement income. Canadians now benefit from expanded flexibility when choosing when to start payments. Claiming as early as age 60 comes with a 0.6% monthly reduction, reaching a maximum cut of 36%, while delaying until age 70 delivers a 0.7% monthly increase, adding up to 42% in extra lifetime benefits.

These changes reflect longer working lives and differing health circumstances. Individuals who continue working after 65 and before 70 can still contribute, earning additional post-retirement credits that raise future payments. Rolled out gradually since 2019, the enhancements increase CPP’s earnings replacement rate from 25% to 33% of average lifetime income for those with 40 years of contributions by 2026.

CPP benefits are indexed to wage growth, helping maintain purchasing power over time. As a result, the maximum monthly CPP pension stands at CAD 1,433 at age 65, while those who defer to 70 may receive up to CAD 2,034 per month. Retirees can earn unlimited income without benefit clawbacks, a notable shift from older rules.

Applications are handled through My Service Canada Account, with many Canadians enrolled automatically using tax data. Benefits are reviewed regularly to reflect life changes such as spousal death or transitions to disability benefits.

Old Age Security Changes: Deferral Options and the Age-75 Increase

Old Age Security (OAS), Canada’s residency-based senior benefit, also gained new flexibility under the 2026 rules. Eligible seniors can now choose to defer OAS for up to five years, earning a 0.6% monthly increase, equal to a 36% boost if payments begin at age 70.

This deferral option complements the existing 10% OAS increase for seniors aged 75 and over, first introduced in 2022 and continuing through 2026. The adjustment recognizes higher living costs associated with longer life expectancy.

Eligibility depends on Canadian citizenship or legal residency for at least 10 years after age 18, or 20 years for those living abroad. OAS payments are non-contributory and taxable, issued on a bi-monthly basis and indexed quarterly. For January to March 2026, base rates are CAD 727.67 for ages 65–74 and CAD 800.44 for those 75 and older, with further adjustments expected in July based on CPI.

Deferring OAS can be advantageous for individuals with workplace pensions or continued income, locking in permanently higher payments. When combined with the Guaranteed Income Supplement (GIS), qualifying seniors can receive over CAD 2,000 per month in total support.

CPP and OAS Payment Timing Throughout 2026

Reliable payment schedules support the updated system. CPP payments are issued on the 15th of each month, or the previous business day if it falls on a weekend or holiday. OAS payments follow either the 2nd or 15th of the month, depending on birth year.

Direct deposit ensures faster access, typically by the next business day, while mailed cheques may take five to seven days to arrive.

| Quarter / Month | CPP Pension Payment Date | OAS Payment Dates (Cycle 1 & Cycle 2) | Maximum Monthly Amount (CAD – Age 65 / Age 75+) |

|---|---|---|---|

| January – March 2026 | 15th se pehle deposit | 29 Jan / 30 Jan 28 Feb / 1 Mar 27 Mar / 28 Mar |

1,433 / 800.44 |

| April – June 2026 | Har mahine 15 tareekh ya usse pehle | 29 Apr / 30 Apr 28 May / 30 May 27 Jun / 30 Jun |

Quarterly inflation index ke mutabiq |

| July – September 2026 | 15th se pehle direct deposit | 29 Jul / 30 Jul 28 Aug / 29 Aug 25 Sep / 26 Sep |

CPI ke hisaab se revised increase |

| October – December 2026 | 15 tareekh se pehle payment clear | 29 Oct / 30 Oct 27 Nov / 28 Nov 20 Dec / 22 Dec |

Year-end final adjustment |

How Claiming Timing Affects Lifetime Retirement Income

The expanded flexibility highlights clear trade-offs. Starting CPP at age 60 results in an estimated CAD 968 per month, reflecting a 32% reduction from the standard age-65 amount. In contrast, delaying until age 70 raises monthly payments to approximately CAD 2,034, representing a 42% increase.

OAS shows a similar pattern. Deferring from age 65 to 70 increases monthly payments from roughly CAD 727 to about CAD 992, creating a higher guaranteed income for life.

| Claim Age | CPP Monthly (from 1,433 base) | OAS Monthly (from 727 base, 65-74) | Combined Annual Gain/Loss vs Age 65 |

| 60 | CAD 968 (-36%) | N/A | -CAD 7,200 (CPP only) |

| 65 | CAD 1,433 (standard) | CAD 727 | Baseline |

| 70 | CAD 2,034 (+42%) | CAD 992 (+36%, if deferred) | +CAD 13,200 combined |

| 75+ | As above + post-retirement boosts | CAD 800 (+10%) | +CAD 860 extra OAS |

Updated Eligibility Rules and Application Procedures

CPP eligibility requires a minimum of 40 contributory years, with provisions that exclude low-earning periods from calculations. OAS eligibility is based on residency history, with automatic enrolment available for most Canadians through tax filings.

In 2026, My Service Canada Account streamlining allows about 90% of applications to be processed within 30 days. Newcomers qualify for OAS after 10 years of residency, while Canadians abroad must meet a 20-year requirement.

Spousal sharing, survivor benefits, and GIS eligibility are integrated into the system. GIS is automatically assessed for low-income seniors and can provide up to CAD 1,065 per month. Early CPP claims now require health declarations, with appeal processes resolving most cases successfully.

Working While Receiving CPP or OAS

The flexible retirement rules allow beneficiaries to continue working without earnings limits. CPP recipients under 70 must still contribute, generating additional benefit credits that raise future payments.

OAS imposes no work restrictions, although incomes above CAD 90,000 are subject to a 15% recovery tax. These rules support phased retirement, with a majority of Canadians aged 65–69 combining part-time work and benefits. Tax integration through RRSP adjustments helps preserve incentives.

Inflation Protection and Maximum Benefit Levels in 2026

Both programs are protected through quarterly CPI indexing. OAS typically increases by 2–3% during annual adjustments, while CPP maximums reflect the completed enhancement.

In 2026, the CPP ceiling remains CAD 1,433 at age 65, with higher amounts available for those who defer. GIS payments rise alongside inflation and remain non-taxable.

| Benefit | Jan-Mar 2026 Max | Projected Jul-Sep 2026 (2.5% CPI) | 75+ Boost |

| CPP | CAD 1,433 | CAD 1,468 | N/A |

| OAS (65-74) | CAD 727.67 | CAD 746 | N/A |

| OAS (75+) | CAD 800.44 | CAD 820 | Included |

Provincial Coordination and Enhanced GIS Support

Provincial programs align with federal benefits. Quebec’s QPP, for example, mirrors CPP rules with comparable enhancements. GIS eligibility thresholds, such as incomes below CAD 21,624 for single seniors, allow combined benefits to exceed CAD 2,500 per month in some cases.

Key Risks and Considerations When Choosing Claiming Ages

Early claiming may suit individuals with shorter life expectancy, while deferral carries the risk of unclaimed benefits in the event of early death. Health status, spousal coordination, and income planning all play important roles.

Long-term projections typically assume longevity beyond age 85, making timing decisions a critical part of retirement planning.

What Lies Ahead After the 2026 Reforms

Looking forward, projections suggest CPP maximums could exceed CAD 2,500 by 2030 as enhancements mature. OAS sustainability continues to rely on population growth and immigration supporting the funding base.

Final Overview

The 2026 CPP and OAS updates introduce a more personalised retirement system, offering meaningful choices between early access and high-value deferral options. With lifetime increases of 36% to 42%, inflation protection, and the ability to work while collecting benefits, these reforms better align retirement income with modern lifespans. Canadians are encouraged to review their My Service Canada Account to make informed decisions and maximise long-term security.